The ISF operated by DHRM provides consolidated services to all state agencies. The ISF has three programs: Field Services, Payroll Field Services, and Legal Services.

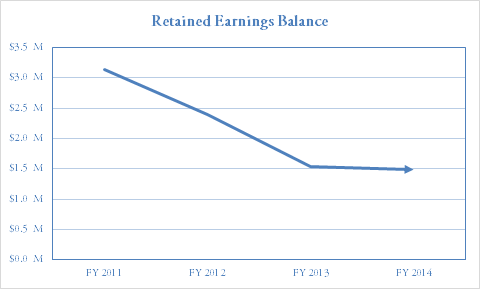

Balanced Retained Earnings

While some retained earnings are necessary for an ISF to cover any unforseen costs fluctuations, the amount of retained earnings itself should not fluctuate much. If retained earnings continually grow or shrink, the ISF is over charging, or under charging, for its services and needs to re-evaluate its rate structure.

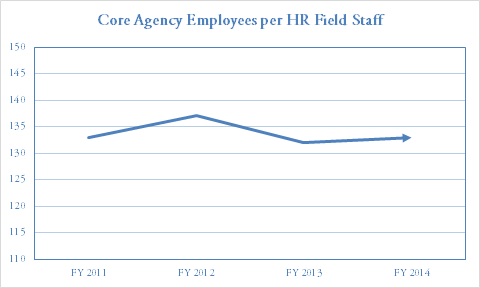

Core Agency Employees per HR Field Staff

In order to measure ISF efficiency, DHRM tracks the ratio of HR field staff to core agency employees. In FY 2014, there was one HR field staff for every 133 core agency employees.

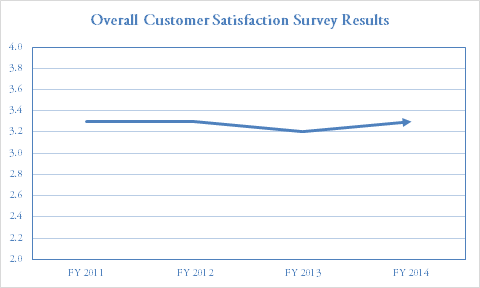

Customer Satisfaction

Every year, DHRM sends out a customer satisfaction survey to the state agencies for which it provides service. This survey is designed to measure how well DHRM is meeting their mission as well as to identify areas for improvement.

In order to control the size, mission and fees charged to state agencies, the Legislature imposed statutory controls (UCA 63J-1-410) that require ISFs to respond to the legislative budget process. No ISF can bill another agency for its services unless the Legislature has: approved the ISF's budget request, FTE, capital acquisitions, rates, fees, and other charges; published the annual rates and fees in an appropriations act; and appropriated the ISF's estimated revenue.

Working capital for operations must be provided from the following sources in the following order: 1. Operating revenues, 2. Long-term debt, and 3. Appropriations from the Legislature.

To eliminate negative working capital, an ISF may borrow from the General Fund as long as the debt is repaid over the useful life of the asset and the deficit working capital is greater than ninety percent of the value of the ISF's fixed assets.

Rates are based on a detailed analysis of the costs of providing human resource functions statewide. The intent behind creation of the ISF was to save money or at worst be revenue neutral with improved coordination and control.

COBI contains unaudited data as presented to the Legislature by state agencies at the time of publication. For audited financial data see the State of Utah's Comprehensive Annual Financial Reports.