Agency: Administrative Services Line Item: Finance Administration Function The Division of Finance is the State of Utah's central financial accounting office. The division provides direction regarding fiscal matters, financial systems, processes and information. This includes maintaining accounting and payroll systems, ensuring compliance with state financial laws, maintaining a data warehouse of financial information, producing the state's financial reports, and processing the state's payments.

The Division of Finance is divided into six programs (Director, Payroll, Payables/Disbursing, Technical Services, Financial Reporting, and Financial Information Systems) to accomplish its mission. Some of its key functions are to: - Produce the State's Comprehensive Annual Financial Report

- Ensure compliance with generally accepted accounting principles

- Disburse all payments to vendors, contractors, and employees

- Develop, operate, and maintain accounting systems to control spending, state assets, and state loans

- Process the state's payroll

- Account for revenues collected by all agencies

Statutory Authority The following are some of the many statutes governing operations of the Division of Finance: UCA 51-5-2 requires the division to establish procedures for the administration and collection of taxes, licenses, fees, and other revenues to allow them to be credited directly into the funds for which they are designated. UCA 51-5-6 requires the division to use generally accepted accounting principles applicable to government units. The division must follow Governmental Accounting Standards Board standards, calculate liabilities associated with post-employment benefits, post revenues to the appropriate funds, prepare revenue and expenditure statements, and determine ISF costs that are eligible for federal reimbursement. UCA 63A-3 is entitled "Division of Finance." Among its key provisions are: - The division director is the state's chief fiscal officer and the state's accounting officer

- The division must define fiscal procedures, provide accounting controls, approve proposed expenditures, establish procedures to account for leases, and prepare financial reports for the state auditor�s examination. Higher Education institutions are subject to this statute only to the extent required by the Board of Regents.

- The director must establish per diem rates for all state officers and employees of the executive branch, except higher education

- The director must adopt rules governing in-state and out-of-state travel by employees of the executive branch, except higher education

- The director must appoint an accounting officer and other officers necessary to economically perform the functions of the division. The director must also establish a comprehensive state accounting system and exercise accounting control over all state agencies except higher education

- The director must maintain a financial control system according to generally accepted accounting principles, to include keeping accounts in balance and giving the governor and legislature reports

- The division must collect accounts receivable as described in UCA 63A-3-Part 3

Intent Language Under Section 63J-1-603 of the Utah Code the Legislature intends that appropriations provided for Finance Administration in Item 17 of Chapter 3 Laws of Utah 2011 not lapse at the close of Fiscal Year 2012. The use of any nonlapsing funds is limited to the following: maintenance and operation of statewide systems and websites, studies, training, and information technology support and hardware - $1,750,000. Funding Detail Financing from the General Fund Restricted -- ISF Overhead account represents charges to the internal service funds for overhead services such as accounting and auditing, building space, maintenance, security, etc. These funds are used in the Financial Information Systems program for FINET (statewide accounting system) support. Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $6,369,900 | $5,983,800 | $5,512,200 | $5,496,300 | $5,959,000 | | General Fund, One-time | $277,900 | ($179,400) | $38,400 | $50,000 | $285,000 | | Transportation Fund | $450,000 | $450,000 | $450,000 | $450,000 | $450,000 | | Dedicated Credits Revenue | $1,836,700 | $1,818,100 | $1,921,400 | $1,391,800 | $1,395,700 | | GFR - ISF Overhead | $1,299,600 | $1,299,600 | $1,299,600 | $1,299,600 | $1,299,600 | | Beginning Nonlapsing | $1,372,300 | $1,285,900 | $1,385,400 | $1,355,000 | $474,200 | | Closing Nonlapsing | ($1,285,900) | ($1,385,400) | ($1,355,000) | ($1,295,500) | $0 | | Lapsing Balance | $0 | $0 | $0 | ($42,000) | $0 | | Total | $10,320,500 | $9,272,600 | $9,252,000 | $8,705,200 | $9,863,500 |

|---|

| | | | | | Programs:

(click linked program name to drill-down) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Finance Director's Office | $396,600 | $441,400 | $462,600 | $475,600 | $655,900 | | Payroll | $2,009,000 | $1,920,700 | $1,738,000 | $1,768,300 | $1,858,000 | | Payables/Disbursing | $2,112,400 | $2,003,500 | $1,817,000 | $1,449,900 | $1,694,300 | | Technical Services | $1,301,000 | $801,600 | $1,070,300 | $897,400 | $1,104,800 | | Financial Reporting | $1,561,600 | $1,559,900 | $1,495,800 | $1,465,300 | $1,746,000 | | Financial Information Systems | $2,939,900 | $2,545,500 | $2,668,300 | $2,648,700 | $2,804,500 | | Total | $10,320,500 | $9,272,600 | $9,252,000 | $8,705,200 | $9,863,500 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $4,744,200 | $4,655,000 | $4,386,000 | $4,209,200 | $4,729,400 | | In-state Travel | $700 | $3,200 | $1,100 | $900 | $1,300 | | Out-of-state Travel | $11,700 | $3,600 | $12,400 | $6,400 | $8,200 | | Current Expense | $881,600 | $1,645,400 | $825,100 | $630,800 | $594,100 | | DP Current Expense | $4,035,600 | $2,864,400 | $3,901,200 | $3,857,900 | $4,280,500 | | DP Capital Outlay | $646,700 | $101,000 | $126,200 | $0 | $0 | | Other Charges/Pass Thru | $0 | $0 | $0 | $0 | $250,000 | | Total | $10,320,500 | $9,272,600 | $9,252,000 | $8,705,200 | $9,863,500 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 57.0 | 53.0 | 55.0 | 53.0 | 56.0 | | Actual FTE | 54.7 | 54.1 | 48.9 | 47.1 | 0.0 |

|

|

|

|

|

|

|---|

Subcommittee Table of ContentsProgram: Finance Director's Office Function The director of the Division of Finance is the state's chief fiscal officer and is responsible for the accounting structure within state government. This includes: - Procedures for the approval and allocation of funds

- Accounting control over fund assets

- Procedures for approval of proposed expenditures

- Statewide payroll and accounting policies

- Financial reporting

- Budgetary compliance monitoring

The director is also responsible for directing and maintaining a financial control system in accordance with generally accepted accounting principles. (UCA 63A-3-204.) Funding Detail Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $396,600 | $404,700 | $459,800 | $395,100 | $405,900 | | General Fund, One-time | $0 | $203,300 | $0 | $50,000 | $250,000 | | Dedicated Credits Revenue | $0 | $0 | $2,800 | $0 | $0 | | Beginning Nonlapsing | $0 | $0 | $166,600 | $166,600 | $0 | | Closing Nonlapsing | $0 | ($166,600) | ($166,600) | ($136,100) | $0 | | Total | $396,600 | $441,400 | $462,600 | $475,600 | $655,900 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $373,300 | $416,800 | $440,500 | $452,000 | $345,800 | | In-state Travel | $0 | $2,800 | $900 | $700 | $800 | | Out-of-state Travel | $2,400 | $2,500 | $1,700 | $1,800 | $1,700 | | Current Expense | $15,100 | $12,900 | $13,100 | $13,300 | $51,500 | | DP Current Expense | $5,800 | $6,400 | $6,400 | $7,800 | $6,100 | | Other Charges/Pass Thru | $0 | $0 | $0 | $0 | $250,000 | | Total | $396,600 | $441,400 | $462,600 | $475,600 | $655,900 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 3.0 | 3.0 | 3.0 | 3.0 | 2.0 | | Actual FTE | 3.0 | 3.7 | 4.0 | 4.1 | 0.0 |

|

|

|

|

|

|

|---|

Subcommittee Table of ContentsProgram: Payroll Function The Payroll program is responsible for maintaining and operating the state's time and attendance and payroll systems. This program develops and delivers payroll policy, procedures, training, and a variety of reports and files including: - Payroll registers

- Utah Retirement Systems reports

- Detail labor distribution files

- General ledger journal vouchers

- Various federal reports

Payroll services include collecting and processing employee time, calculating gross and net pay, calculating benefits, payments to employees, payments to third parties (such as benefit providers, taxing authorities, and employee associations), calculating and distributing labor costs that are passed to the state's financial systems and data warehouse, adhering to federal and state employment laws and regulations, and maintaining current and historical employee and payroll data. The program also oversees Employee Self-Service (ESS), a payroll and time processing system that allows employees to enter their time on-line, view their own payroll data, and update certain information such as W-4 forms without involving a payroll technician. This system has reduced administration costs and improved employee satisfaction. Funding Detail Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $1,870,600 | $1,812,300 | $1,682,800 | $1,643,400 | $1,692,800 | | General Fund, One-time | $0 | ($268,800) | $0 | $0 | $0 | | Dedicated Credits Revenue | $90,900 | $91,100 | $90,200 | $90,300 | $90,200 | | Beginning Nonlapsing | $428,600 | $381,100 | $95,000 | $130,000 | $75,000 | | Closing Nonlapsing | ($381,100) | ($95,000) | ($130,000) | ($95,400) | $0 | | Total | $2,009,000 | $1,920,700 | $1,738,000 | $1,768,300 | $1,858,000 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $570,600 | $577,800 | $478,400 | $484,800 | $493,100 | | In-state Travel | $300 | $0 | $0 | $0 | $0 | | Out-of-state Travel | $2,000 | $0 | $3,400 | $3,000 | $3,400 | | Current Expense | $17,100 | $12,700 | $15,500 | $14,100 | $33,500 | | DP Current Expense | $1,238,100 | $1,243,600 | $1,235,700 | $1,266,400 | $1,328,000 | | DP Capital Outlay | $180,900 | $86,600 | $5,000 | $0 | $0 | | Total | $2,009,000 | $1,920,700 | $1,738,000 | $1,768,300 | $1,858,000 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 7.0 | 4.0 | 6.0 | 4.0 | 6.0 | | Actual FTE | 7.7 | 7.9 | 6.1 | 6.0 | 0.0 |

|

|

|

|

|

|

|---|

Subcommittee Table of ContentsProgram: Payables/Disbursing Function This program: - Audits payment and employee reimbursement requests

- Manages the FINDER collections program

- Manages vendor information in FINET

- Manages all checks redeemed by the bank

- Provides information to the public and other agencies about the status of lost, missing, or cashed checks

- Distributes tax money to cities and counties

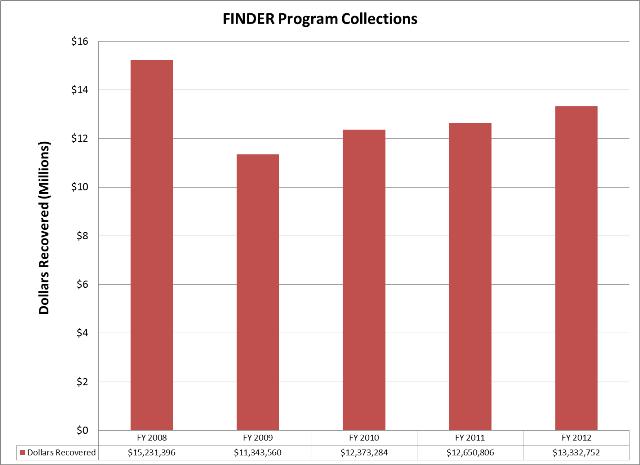

Finance manages a program called FINDER with the aim of improving the collection of funds owed to the state. The program matches tax refunds and vendor payments with outstanding receivables due the State. Those receivables include tax bills, child support, student loans, parking and moving violations, and unemployment insurance. If a match is made, the payment or tax refund is intercepted and paid to the entity. This function is fully funded by the administrative fees collected as debts are paid ($15 per transaction). The disbursement function handles the mailing and distribution of all centrally processed payments including electronic fund transfers and checks mailed for such things as vendor payments, tax refunds, and payroll. Since the 2000 General Session, the Legislature has asked the Department of Administrative Services to follow a mileage reimbursement program. This program requires agencies to reimburse employees for personal vehicle use at one of two levels: (1) if a state motor pool vehicle is available, employees are reimbursed at a rate equal to, or less than, the per mile cost of a mid-size sedan operated by the Division of Fleet Operations; (2) if a state motor pool vehicle is unavailable, employees are reimbursed at a higher rate tied to IRS approved rates. The goal of the mileage reimbursement program is to encourage employees to use vehicles already in the state motor pool. When employees request reimbursement for using a personal vehicle on long trips, the state pays for a vehicle twice -- once for the employee's mileage and again for the unused state vehicle. As gasoline prices and maintenance costs rise, the cost of operating a state sedan rises and the reimbursement rate is adjusted accordingly. The division also adjusts its reimbursement rates annually to match IRS approved rates. Performance The Division strives to improve the collection of funds owed to the state.  Funding Detail Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $862,000 | $928,000 | $613,800 | $889,600 | $931,100 | | General Fund, One-time | $66,200 | ($114,700) | $0 | $0 | $0 | | Dedicated Credits Revenue | $1,184,200 | $1,190,200 | $1,298,100 | $779,000 | $763,200 | | Beginning Nonlapsing | $0 | $0 | $0 | $94,900 | $0 | | Closing Nonlapsing | $0 | $0 | ($94,900) | ($271,600) | $0 | | Lapsing Balance | $0 | $0 | $0 | ($42,000) | $0 | | Total | $2,112,400 | $2,003,500 | $1,817,000 | $1,449,900 | $1,694,300 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $1,296,700 | $1,230,200 | $1,047,600 | $907,400 | $1,214,700 | | In-state Travel | $400 | $400 | $0 | $200 | $300 | | Out-of-state Travel | $1,800 | $0 | $2,200 | $1,100 | $1,000 | | Current Expense | $772,500 | $728,500 | $724,900 | $508,400 | $442,100 | | DP Current Expense | $41,000 | $44,400 | $42,300 | $32,800 | $36,200 | | Total | $2,112,400 | $2,003,500 | $1,817,000 | $1,449,900 | $1,694,300 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 17.0 | 17.0 | 17.0 | 17.0 | 17.0 | | Actual FTE | 18.8 | 16.9 | 14.0 | 12.6 | 0.0 |

|

|

|

|

|

|

|---|

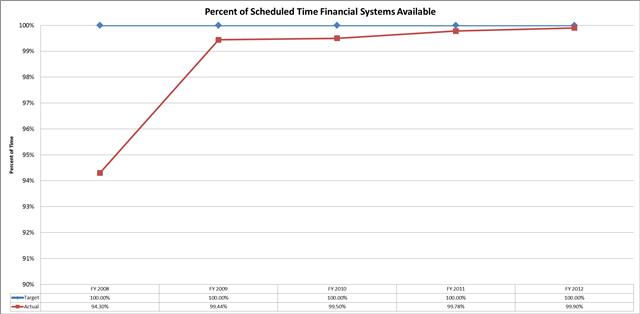

Subcommittee Table of ContentsProgram: Technical Services Function This program provides support for various division systems and hardware including the statewide payroll system and the statewide accounting system, FINET. In addition, this section is responsible for the creation and maintenance of the division's data warehouse, which contains current and historical financial, personnel, and payroll information. Its mission is to develop the computer tools that will enable personnel in state agencies to access the division's data warehouse and to provide the information needed by agency financial managers. Access to quality financial information should enhance the ability of managers to make sound business decisions. It has resulted in a reduction of printed reports and the amount of time needed. This information is available in a variety of ways, including the Internet. Managers and financial analysts statewide run thousands of queries against the data warehouse each month. The data warehouse is reviewed annually by the State Auditor's Office and has been determined to contain reliable data. Performance Data warehouse should provide agencies the tools they need to access

accurate, current, and historical information from the financial, human

resource, and payroll systems. Unscheduled down time should be minimized.  Funding Detail Due to IT consolidation, the Technical Services section staff is now part of the Department of Technology Services, effective FY 2007. Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $1,091,000 | $832,700 | $943,200 | $683,900 | $902,200 | | General Fund, One-time | $0 | $227,300 | $38,400 | $0 | $35,000 | | Beginning Nonlapsing | $253,900 | $43,900 | $302,300 | $213,600 | $167,600 | | Closing Nonlapsing | ($43,900) | ($302,300) | ($213,600) | ($100) | $0 | | Total | $1,301,000 | $801,600 | $1,070,300 | $897,400 | $1,104,800 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Current Expense | $0 | $796,100 | $0 | $700 | $0 | | DP Current Expense | $957,600 | $5,500 | $949,100 | $896,700 | $1,104,800 | | DP Capital Outlay | $343,400 | $0 | $121,200 | $0 | $0 | | Total | $1,301,000 | $801,600 | $1,070,300 | $897,400 | $1,104,800 |

|---|

Subcommittee Table of ContentsProgram: Financial Reporting Function Financial Reporting issues the Comprehensive Annual Financial Report (CAFR) to financial managers in other states, bond rating agencies, financial institutions, the public, and managers within state government. In addition, it sets accounting standards and policies to ensure compliance with state law and generally accepted accounting principles. This program provides information for marketing long term debt (bond sales) and monitors compliance with SEC regulations. Financial Reporting provides service in the following areas: - Cash management: calculates and reports interest earnings and comply with federal cash regulations

- Loans receivable: accounts for and services loans that fund water quality and development projects, low income housing, and community development

- Revenue accounting: establishes and monitors detailed state revenue reporting

- Payment tracking: reconciles all warrants with bank statements and the treasurer's system

- Fixed asset tracking: maintains and monitors the statewide Fixed Asset System

The division provides electronic versions of the CAFR on its website. Performance This program should close each fiscal year and issue the CAFR in a timely manner. Measures for a successful CAFR include receiving an unqualified audit opinion and a certificate of achievement from the Governmental Finance Officers Association (GFOA). These two measures help the state maintain its reputation as a well-managed state and keep its "AAA" bond rating. The Division of Finance has received an unqualified audit opinion as well as a GFOA Certificate of Achievement for its CAFR every year for the last 27 years. Funding Detail During the 2005 General Session, the Legislature funded a $50,000 actuarial study to determine the state's liability for "other post-employment benefits" (paid health insurance in exchange for unused sick leave). The Legislature further added $25,000 in ongoing funds to the budget to repeat the actuarial study every two years as required by the Governmental Accounting Standards Board (GASB). Dedicated Credits pay for accounting services. Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $1,033,400 | $1,239,500 | $957,800 | $1,004,800 | $1,182,000 | | General Fund, One-time | $86,700 | ($315,200) | $0 | $0 | $0 | | Dedicated Credits Revenue | $496,600 | $524,600 | $522,000 | $522,500 | $534,000 | | Beginning Nonlapsing | $171,900 | $227,000 | $116,000 | $100,000 | $30,000 | | Closing Nonlapsing | ($227,000) | ($116,000) | ($100,000) | ($162,000) | $0 | | Total | $1,561,600 | $1,559,900 | $1,495,800 | $1,465,300 | $1,746,000 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $1,480,400 | $1,452,800 | $1,414,300 | $1,357,900 | $1,657,900 | | In-state Travel | $0 | $0 | $200 | $0 | $200 | | Out-of-state Travel | $0 | $0 | $1,000 | $500 | $1,000 | | Current Expense | $52,100 | $77,300 | $49,800 | $79,300 | $49,800 | | DP Current Expense | $29,100 | $29,800 | $30,500 | $27,600 | $37,100 | | Total | $1,561,600 | $1,559,900 | $1,495,800 | $1,465,300 | $1,746,000 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 17.0 | 16.0 | 17.0 | 16.0 | 18.0 | | Actual FTE | 15.0 | 15.6 | 14.8 | 14.4 | 0.0 |

|

|

|

|

|

|

|---|

Subcommittee Table of ContentsProgram: Financial Information Systems Function The Financial Information Systems group maintains the state central accounting system (FINET) and is responsible for coordinating incoming financial data, processing the information, generating warrants, and distributing reports to the departments each month. This section is also responsible for: - User coordination among all state agencies

- Training

- Maintaining and operating the Tax and Wage Garnishments systems

- Maintaining and operating the state Warrant and Electronic Funds Transfer (EFT) Payment System

- Developing, testing, and implementing changes and upgrades to the Unclaimed Property System

- Developing, testing, and implementing changes and upgrades to the Check Writer System that prints warrants for agencies outside of the Division of Finance

Special Funds Overhead charges are allocated to the Internal Service Funds (ISF) for benefits received from other state agencies such as accounting and auditing services, building space, maintenance, security, etc. The overhead payments had been transferred back to the respective ISF as contributed capital that reduced retained earnings and increased contributed capital by the same amount. However, since FY 1994, the revenue received from overhead charges has been transferred to Finance to support the FINET accounting system. Funding Detail Because of the large amount of data processed for the Department of Transportation, a portion of this program is funded from the Transportation Fund. Sources of Finance

(click linked fund name for more info) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp | | General Fund | $1,116,300 | $766,600 | $854,800 | $879,500 | $845,000 | | General Fund, One-time | $125,000 | $88,700 | $0 | $0 | $0 | | Transportation Fund | $450,000 | $450,000 | $450,000 | $450,000 | $450,000 | | Dedicated Credits Revenue | $65,000 | $12,200 | $8,300 | $0 | $8,300 | | GFR - ISF Overhead | $1,299,600 | $1,299,600 | $1,299,600 | $1,299,600 | $1,299,600 | | Beginning Nonlapsing | $517,900 | $633,900 | $705,500 | $649,900 | $201,600 | | Closing Nonlapsing | ($633,900) | ($705,500) | ($649,900) | ($630,300) | $0 | | Total | $2,939,900 | $2,545,500 | $2,668,300 | $2,648,700 | $2,804,500 |

|---|

| | | | | | Categories of Expenditure

(mouse-over category name for definition) | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Personnel Services | $1,023,200 | $977,400 | $1,005,200 | $1,007,100 | $1,017,900 | | Out-of-state Travel | $5,500 | $1,100 | $4,100 | $0 | $1,100 | | Current Expense | $24,800 | $17,900 | $21,800 | $15,000 | $17,200 | | DP Current Expense | $1,764,000 | $1,534,700 | $1,637,200 | $1,626,600 | $1,768,300 | | DP Capital Outlay | $122,400 | $14,400 | $0 | $0 | $0 | | Total | $2,939,900 | $2,545,500 | $2,668,300 | $2,648,700 | $2,804,500 |

|---|

| | | | | | | Other Indicators | 2009

Actual | 2010

Actual | 2011

Actual | 2012

Actual | 2013

Approp |

|---|

| Budgeted FTE | 13.0 | 13.0 | 12.0 | 13.0 | 13.0 | | Actual FTE | 10.3 | 10.0 | 10.0 | 10.0 | 0.0 |

|

|

|

|

|

|

|---|

Subcommittee Table of Contents |