The Department of Alcoholic Beverage Control was created by statute in 1935. The Department is charged with the responsibility of conducting, licensing and regulating the sale of alcoholic beverages in a manner and at prices which reasonably satisfy the public demand and protect the public interest.

Liquor sales provide close to $90 million annually to the State's General Fund. Net profits are deposited in the General Fund and used to support state government operations. State law also requires a transfer of 10% of gross sales to support the school lunch program and 1% to the Department of Public Safety to support alcohol-related law enforcement officers. A portion of the tax on beer goes to local governments to help cover their costs of liquor law enforcement.

During the 2015 General Session, the Legislature appropriated for Fiscal Year 2016, $41,153,800 from all sources for DABC Operations. This is a 1.5 percent increase from Fiscal Year 2015 revised estimated amounts from all sources.

In addition to statewide compensation and internal service fund cost increases, the following appropriation adjustments were made during the 2015 General Session:

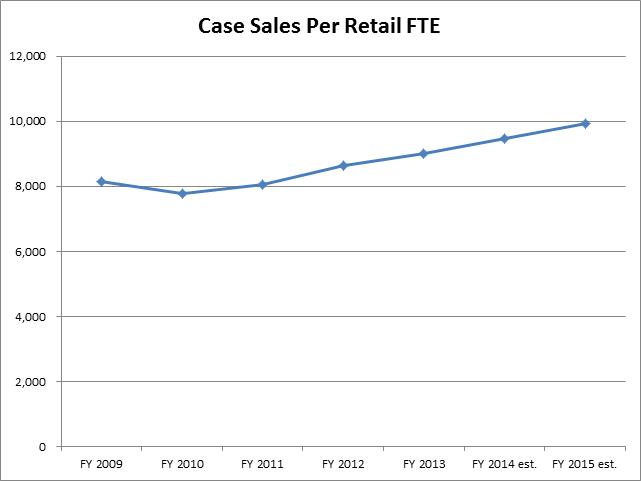

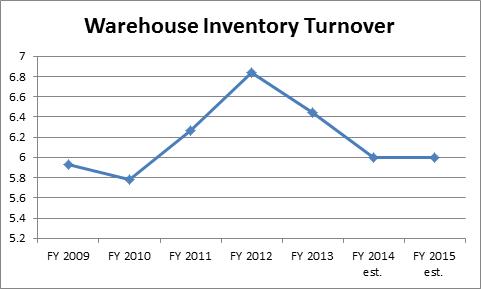

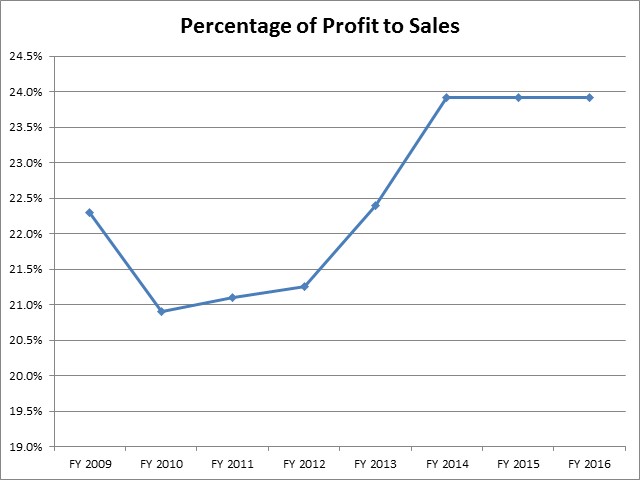

The Department of Alcoholic Beverage Control measures case sales per FTE, warehouse inventory turnover, and percent of profits to sales as performance measures. Data is shown below.

The main DABC line item, Alcoholic Beverage Control, contains the following programs: Executive Director, Administration, Operations, Warehouse & Distribution, and Stores & Agencies.

COBI contains unaudited data as presented to the Legislature by state agencies at the time of publication. For audited financial data see the State of Utah's Comprehensive Annual Financial Reports.